What Is Subrogation in a Texas Personal Injury Case?

Subrogation is a legal term used when an insurance company obtains the right to seek reimbursement after it has paid your bills. In a Texas personal injury case, this usually happens after you are hurt in an accident and your health insurance, auto insurance, or another insurance plan pays for your medical care.

If a third party (like the driver who caused your crash) is responsible for your injuries, your insurer may want to be repaid from your settlement or court award. This means your personal injury settlement could be smaller than you expected.

Many people do not know about subrogation rights until they get told that part of their compensation will go to an insurer or provider. This makes it very important to learn what subrogation is and how it works in Texas.

What Is Subrogation?

Subrogation is a legal right that allows an insurance company or another entity that paid your bills after an injury to seek reimbursement from the responsible person or their insurer. In simple terms, the insurer can “step into your shoes” and seek repayment from the party at fault in a Texas personal injury case.”

Here is how it works in most personal injury claims:

- You are injured in an accident caused by someone else.

- Your health insurance or auto insurance pays for your medical care or other expenses first.

- After you win a settlement or court award, the insurer may ask to be repaid for what it already paid.

This repayment right may include amounts paid for medical bills, property damage, and other accident costs.

In many cases, your insurer will try to get back the money from your personal injury settlement or award rather than making you pay out of pocket. If your settlement is large enough, the insurer’s claim could reduce the net recovery you receive.

In Texas, subrogation rights apply to several types of insurance, including:

- Health insurance plans, including private, employer-sponsored, Medicare, and Medicaid.

- Auto insurance, such as Personal Injury Protection (PIP) or MedPay in some policies.

- Workers’ compensation and other benefits are paid on your behalf.

The insurer’s goal is to make sure the party that caused your injury ultimately bears the cost, rather than the insurer paying for it themselves. But this also means your actual compensation may be smaller after subrogation claims are paid from your recovery.

How Subrogation Works in a Texas Personal Injury Case

When you are hurt in a personal injury claim in Texas, subrogation comes after your insurance pays your bills. An insurance company, health insurance plan, or another entity that paid for your care may want to be repaid from your settlement or court award.

Here is a step-by-step process of how subrogation usually works:

- Accident and Care – You are injured because of someone else’s fault (like a car accident). You get medical treatment, and your health insurance or auto insurance may pay your medical bills.

- Insurance Pays Bills – Your plan (for example, a private health insurance plan, ERISA plan, or MedPay coverage) will pay for the care you received.

- Insurer Checks for Subrogation – After paying your bills, your insurer looks to recover the money from the responsible party or their insurer.

- Notification of Subrogation – The insurer usually notifies you or your attorney that it plans to seek reimbursement or enforce its subrogation rights.

- Reimbursement Demand – The insurer may send a demand or place a subrogation lien against your settlement or award.

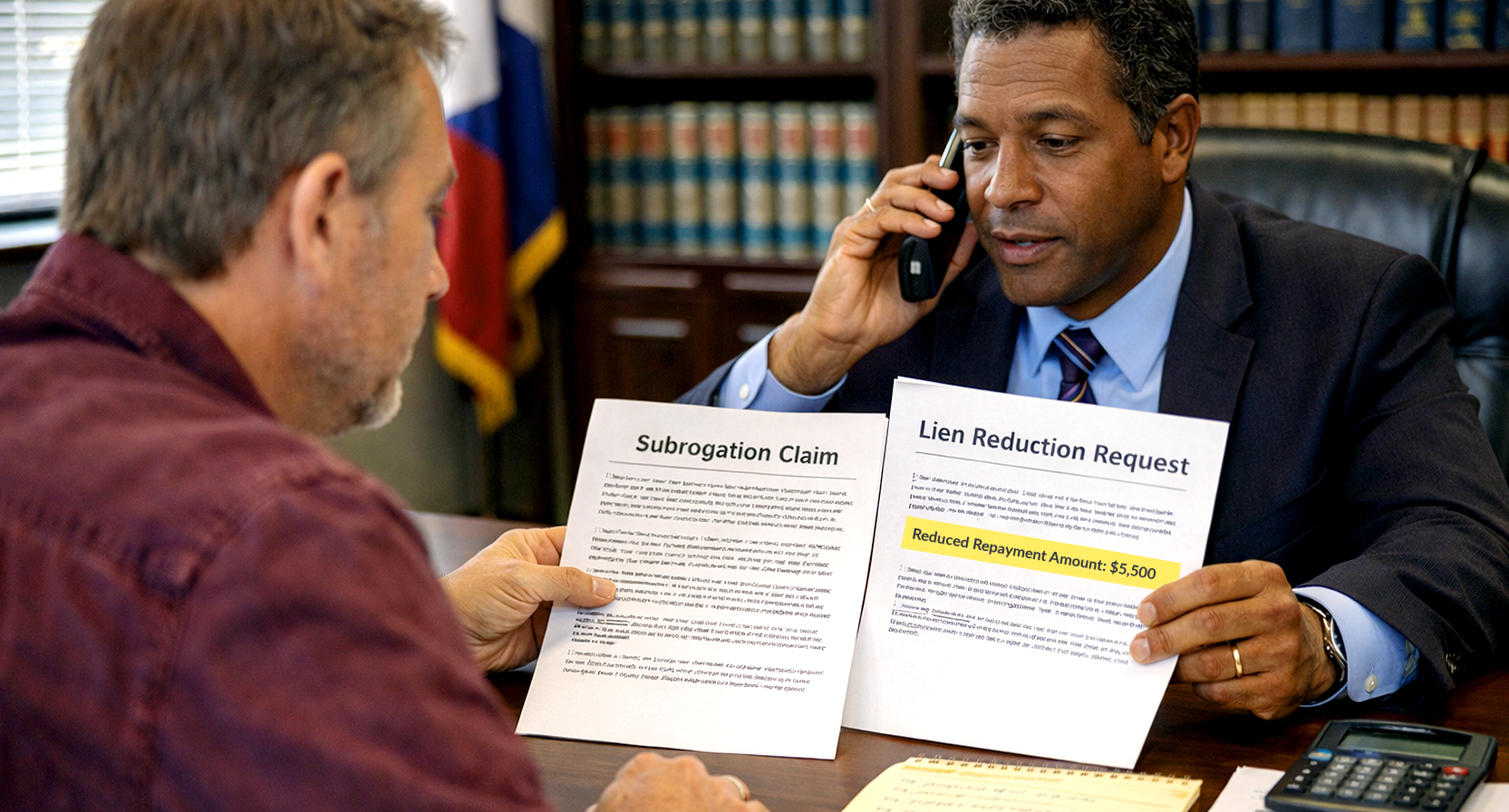

- Negotiation or Repayment – Your lawyer may work with the insurer to negotiate the amount owed or resolve the lien before your settlement is paid out.

In Texas, the process can involve several types of insurers or plans, including health insurance, auto insurance, and, sometimes, workers’ compensation carriers when a third party caused your injuries.

This process works so that the party who caused the injury ultimately pays the costs, not the insurer. But it can also mean your net recovery from the case is lower because part of your settlement may go to repay what was already paid on your behalf.

Texas Law & Subrogation Rules

In Texas personal injury cases, subrogation and reimbursement rights are shaped by state law and special rules that decide when and how an insurance company, health plan, or another entity can seek repayment from your settlement or court award.

Legal Rules in Texas

Texas Civil Practice & Remedies Code Chapter 140 lets an issuer of a health plan or medical benefits contract include subrogation and reimbursement rights in its agreement with you. This means your insurer can be contractually subrogated to recover what it paid for your injury from your recovery against a third party.

Texas law also sets a statute of limitations for many subrogation claims. For example, an insurer typically must assert its rights within two years of the accident date for both property damage and personal injury subrogation claims.

Under Texas common law, the anti-subrogation rule generally stops an insurer from suing its own insured or co-insured under the same policy. A waiver of subrogation clause in a contract can also prevent certain insurers or payors from seeking any repayment.

Hospital & Provider Liens

In addition to insurer subrogation rights, hospital liens are common in Texas personal injury cases. A hospital that treats you after an accident may file a lien on your personal injury cause of action, settlement, or judgment. These liens must be recorded properly under Chapter 55 of the Texas Property Code and typically apply to emergency services provided within a set time after your injury.

These hospital liens are a form of legal claim against your recovery and can reduce your net personal injury settlement if they are not resolved before funds are paid out.

Auto Insurance Subrogation Limits

Texas also has special limits on subrogation rights under certain auto insurance coverages. For example, Personal Injury Protection (PIP) benefits are generally protected from subrogation by statute, unless your policy explicitly allows it and other legal conditions are met.

Similarly, MedPay coverage in auto insurance may be subject to subrogation only if your policy includes those rights.

Exceptions to Subrogation Rules

Some insurance and benefit plans are not fully governed by Texas subrogation rules. These include:

- ERISA plans (employer-sponsored health plans governed by federal law)

- Government programs like Medicare and Medicaid (they have their own reimbursement processes)

- Workers’ compensation claims subrogating against third-party recoveries

These exceptions can change how or when subrogation or repayment applies to your claim or settlement.

Impact of Subrogation on Your Settlement

When subrogation comes up in a personal injury case, it can reduce your net recovery from a personal injury settlement. This is because an insurance company, health plan, or other entity that paid your bills after an accident often has the right to seek reimbursement from the settlement or court award you receive.

How Subrogation Affects Your Money

If your health insurance or other insurance carrier paid for your medical care or other costs, they may file a subrogation lien or make a subrogation claim against your settlement. This means part of what you recover in your personal injury claim may go to repay the insurer instead of reaching your pocket.

For example, if your insurer paid $15,000 in medical expenses and you later receive a $75,000 settlement, the $15,000 could be recouped before you receive your share. That can make your final net recovery much smaller than the headline settlement number.

Why This Happens

Subrogation exists because Texas law and insurance policies allow insurers to step into your legal rights and recover money from the party that caused your accident. This ensures the at-fault driver or their insurer ultimately pays the costs, not your insurer.

Order of Payments Matters

In many injury cases, several claims may attach to your settlement before you see any funds. These can include:

- Attorney fees and case costs

- Valid subrogation liens from insurers or plans

- Hospital or medical provider liens

- Government program reimbursements

These claims are often paid in a set order, and you typically receive money only after they are resolved.

Settlement Example

A settlement may look large on paper, but much smaller once all valid claims are paid. For instance:

- Settlement: $75,000

- Subrogation lien: $15,000

- Other liens and costs: $10,000

Your actual payout can be far less than the original amount offered.

Why an Attorney Matters

A personal injury attorney can help protect your net personal injury settlement by:

- Identifying all potential subrogation rights and liens early

- Reviewing whether the subrogation demand is valid or excessive

- Negotiating with insurers to reduce repayment amounts

- Ensuring your settlement allocation considers all claims fairly

Understanding how subrogation works and how it affects your settlement helps you avoid surprises and plan for how much money you’ll actually take home after a Texas personal injury case.

Can Subrogation Claims Be Negotiated?

In a Texas personal injury case, subrogation claims and subrogation liens are often negotiable. This means you and your personal injury attorney can talk with the insurance company or other payors to try to lower the amount they want to be repaid from your personal injury settlement.

Yes, Subrogation Can Be Negotiated

If your health insurance, auto insurer, or another entity demands repayment, you do not always have to pay the full amount they request. A skilled attorney can help negotiate or reduce the amount owed.

How Negotiation Works

Your lawyer can use several strategies to protect your net recovery:

- Hardship Negotiation: If paying the full lien would leave you with little or no settlement money, your lawyer can argue that the insurer should accept a smaller amount because you are not “made whole” yet.

- Attorney Fee Offset: Under Texas law, insurers that benefit from your settlement may need to share in your attorney fees and costs, effectively reducing what they can claim back.

- Limited Settlement Funds: If your total settlement is small, insurers may agree to a proportional repayment rather than take a large share.

- Documentation Review: Your attorney can review subrogation letters and itemized bills to check whether every charge relates to your injury and whether the amounts are reasonable before agreeing to pay them.

Why Negotiation Matters

Subrogation negotiation helps you keep more of your settlement. If your insurer demands full repayment without negotiation, your settlement could be significantly reduced even after legal fees.

Exceptions and Limits

Some types of liens may be harder to reduce:

- Government liens, such as Medicare or Medicaid, follow strict federal rules and may require formal waiver procedures.

- ERISA plans may enforce repayment more strictly than state law alone.

Even with these limits, negotiation is usually possible and often successful when handled by someone experienced in Texas insurance subrogation law and personal injury settlement planning.

Your Rights as an Injured Person

When subrogation comes up in a Texas personal injury case, you have important rights that help protect your net recovery and ensure you are fairly treated under the law. These rights apply whether your health insurance plan, auto insurance, or another entity paid for your medical bills or other damages.

Right to Be Informed

If an insurance company or other payor plans to seek reimbursement or enforce a subrogation claim, they must notify you or your personal injury attorney. This gives you the chance to understand exactly what they are demanding and why.

Right to Full Compensation First

Under the made-whole doctrine in Texas, your insurer often cannot enforce its subrogation rights until you are “made whole,” meaning you have been fully compensated for your losses, including medical expenses, lost wages, and other damages. If you are not fully compensated, the insurer may have to wait or accept a smaller amount.

Right to Challenge Subrogation Claims

You can challenge a subrogation lien or a repayment demand if it is excessive, inaccurate, or unfair. Your attorney can review subrogation letters, check policy language, and argue that the claim should be reduced or waived, especially if your recovery is limited.

Right to Have Subrogation Negotiated

Many subrogation claims are negotiable. This means your attorney can work with the insurance carrier, health plan, or other payor to try to reduce the repayment amount. Negotiations may be based on:

- Your limited settlement amount

- The insurer benefits from your attorney’s work

- Whether you were “made whole” before repayment

Right to Protect Your Net Recovery

Because subrogation rights and liens can reduce what you actually take home from your personal injury settlement, you have the right to protect your net recovery. A skilled attorney will identify all subrogation claims, verify each one, and take steps to minimize how much you pay out of your award. This includes negotiating with:

- Health insurance plans

- Auto insurance carriers

- ERISA-governed plans and government programs like Medicare and Medicaid

- Hospital and provider liens

Right to Legal Help

Subrogation law can be complicated. ERISA reimbursement rules and state limitations may apply, and some payors, like Medicare, have federal lien rules that must be handled properly to avoid bigger problems later. Working with a personal injury attorney helps ensure that your rights are protected and that your settlement planning considers all potential repayment claims.

Common Misconceptions About Subrogation

Many people misunderstand subrogation in a Texas personal injury case. These myths can cause confusion and worry for injured victims. Knowing the truth helps you plan your settlement, protect your net recovery, and avoid surprises.

Misconception 1: Your Settlement Is All Yours

Some people think that when you settle a personal injury claim, the full amount goes to you. The truth is, your compensation may be reduced by subrogation claims from health insurance, auto insurance, or other payors that already paid bills on your behalf.

Misconception 2: Subrogation Only Happens After You Receive Money

It is often assumed that subrogation waits until the settlement is finalized. In reality, insurers start checking subrogation rights while your case is being prepared, and they may file a subrogation lien or make a claim early in the process.

Misconception 3: You Always Have to Pay the Full Amount Back

Many people believe you must pay every dollar the insurer paid. But in many cases, these subrogation claims can be negotiated or reduced if your settlement is not large enough to cover everything without leaving you unfairly harmed.

Misconception 4: Only Health Insurance Can Subrogate

Subrogation is not just about health insurance. Auto insurance (including MedPay and sometimes PIP), workers’ compensation plans, and even medical providers with hospital liens can all seek repayment if they paid your bills after an injury.

Misconception 5: You Cannot Challenge a Subrogation Claim

Some think subrogation claims are final and cannot be contested. In fact, a personal injury attorney can review the claim for errors, negotiate with the insurer, or argue that the insurer must share in attorney fees or accept a lower repayment amount.

Misconception 6: Subrogation Is Unfair or Illegal

Subrogation is a legal right recognized under Texas law. It exists so that the party who caused the injury ultimately pays the costs, rather than your insurer. While it can affect your payout, it is not illegal or inherently unfair when applied correctly.

Misconception 7: Federal Plans Don’t Subrogate

While some think federal plans like Medicare or ERISA health plans never seek repayment, these plans may have their own reimbursement rules. They often require you to repay what they paid if you settle with the at-fault party.

Misconception 8: An Insurance Company Cannot Subrogate If You Cooperate

Failing to cooperate with your insurer’s subrogation efforts can actually make you responsible for the full amount out of your pocket. It is important to comply with reasonable requests to protect your rights and interests.

Knowing the facts about subrogation helps you handle your personal injury recovery more effectively and avoid mistakes that could cost you money.

How a Personal Injury Attorney Helps

A personal injury attorney plays a key role when subrogation affects your Texas personal injury case. These lawyers know how to handle insurance claims, including health insurance, auto insurance, and ERISA reimbursement claims, so you can keep more of your net recovery after a personal injury settlement.

1. Identify All Subrogation and Liens

A good attorney will find every possible subrogation claim and lien against your settlement. This includes:

- Health insurance subrogation or repayment rights

- Hospital liens and provider liens

- Auto insurance liens for MedPay or Med-Pay

- ERISA reimbursement rights from employer plans

- Government program liens like Medicare or Medicaid

Your lawyer reviews all insurance policies and bills, so you know what claims are valid and how they affect your settlement allocation and final payout.

2. Review Policy Language and Legal Rights

Different plans have different rights. For example:

- Some plans have a waiver of subrogation clause that limits repayment

- ERISA plans often have strong ERISA reimbursement rights that look different from Texas law

- Policies may or may not follow the made-whole doctrine

Your attorney reads the policy language and checks whether an insurer can demand money from your personal injury settlement or must share attorney fees and costs.

3. Negotiate Subrogation Claims

Experienced attorneys often negotiate or reduce what insurers say they want. They use arguments such as:

- Your settlement funds are limited

- You were not made whole yet

- The insurer benefited from your attorney’s work, so it should pay part of the fees

These negotiations can reduce or even eliminate large subrogation liens that would take a big bite out of your compensation.

4. Protect Your Net Recovery

Your lawyer focuses on making sure you get the most money possible from your case after all claims are paid. This includes planning how money is paid out, which liens go first, and what portions of your settlement go to subrogation, hospital liens, and your attorney fees.

5. Avoid Legal Problems Later

If subrogation claims are ignored or handled incorrectly, insurers may delay your settlement or even take legal action to get paid. A qualified Dallas or Texas injury attorney handles these issues so you do not face future lawsuits or collection claims related to your case.

In short, hiring a personal injury attorney helps you manage complex subrogation rights, protect your net recovery, and make sure that liens and repayment demands are fair and legally correct.

FAQs About Subrogation in a Texas Personal Injury Case

Here are clear and simple answers to common questions about subrogation and how it may affect your personal injury settlement.

1. Do I Have to Pay My Insurance Company Back?

If your insurance policy has a valid subrogation clause, and your health insurance or auto insurance paid your bills after an accident, the insurer usually has the legal right to be repaid from your settlement or court award. Ignoring a subrogation claim can delay your settlement or lead to other legal problems.

2. What Is a Subrogation Lien?

A subrogation lien is a legal claim the insurance company, health plan, or other payor places on part of your settlement money to secure repayment of what it paid on your behalf. If valid, the lien must be dealt with before your net recovery is released.

3. Can Subrogation Be Reduced or Negotiated?

Yes. A personal injury attorney can often negotiate or reduce the amount your insurer is asking for based on Texas subrogation law, the made whole doctrine, and whether your settlement is limited. Negotiation can increase the amount of money you keep.

4. Does Texas Follow the “Made Whole Doctrine”?

In many cases, Texas law (including common law and statutes such as the Civil Practice & Remedies Code Chapter 140) recognizes the made-whole doctrine, meaning insurers may need to wait until you are fully compensated before collecting onsubrogation. This rule is not absolute and can be affected by your policy terms or plan type.

5. Can Hospital Liens Affect My Settlement Too?

Yes. Hospital liens and other medical provider liens can also attach to your settlement money. These liens are separate from insurer subrogation rights and must be resolved before you receive funds.

6. What Happens if I Ignore a Subrogation Claim?

Ignoring a valid subrogation claim or lien can delay your settlement or lead to lawsuits against you or your attorney. It may also hurt your net recovery and financial planning after your case.

7. Are Subrogation and Reimbursement the Same Thing?

They are related but not always the same. Subrogation often means the insurer steps into your legal rights to seek money from the responsible party, while reimbursement usually means the insurer expects you to repay what it paid from your settlement. Both can reduce your payout.

8. Does Subrogation Only Happen in Auto Accidents?

No. Subrogation can occur in many types of personal injury claims, including car accidents, slip-and-fall injuries, workplace injuries with third-party liability, and more. Any time a third party causes harm, and an insurer pays bills, subrogation rights may arise.

9. Do Government Plans Like Medicare or Medicaid Subrogate?

Yes. Medicare, Medicaid, and similar government programs can seek repayment for what they paid under federal and state rules. Their processes are often stricter and separate from Texas subrogation laws.

10. Can I Fight a Subrogation Claim if It Is Wrong or Too High?

Yes. If the amount is inaccurate, too high, or unfair based on the settlement size, your attorney can challenge it, especially if the insurer did not follow proper legal steps under Texas law.

11. What Should I Do First if I Get a Subrogation Letter?

Keep the notice, share it with your personal injury attorney, and do not ignore it. Early action and good documentation can help protect your net settlement and avoid delays.