Texas Surprise Billing and Balance Billing Rules

Texas’s surprise billing and balance billing rules are about how doctors, hospitals, and other out-of-network providers can charge patients. Balance billing is when a health care provider bills you for the difference between what your insurance plan pays and what the provider charges. It can happen when you go to an in-network facility but see a doctor who is not in your insurance network.

In Texas, state rules and federal law work together to protect people from unexpected medical bills. The No Surprises Act (NSA) is a national rule that stops many kinds of surprise billing. Texas Senate Bill 1264 and parts of the Texas Insurance Code ban certain balance bills for people with state-regulated health plans.

These protections ensure you pay only your plan’s deductible, copay, or coinsurance for emergency care and other services. If a surprise medical bill still shows up, you can ask for help through a process like Independent Dispute Resolution (IDR) or a mediation or arbitration process.

What Is Surprise Billing vs. Balance Billing

Surprise billing and balance billing are ways you might get an unexpected medical bill from a health care provider. Balance billing is when a provider bills you for the amount insurance does not pay. This happens when the provider is out-of-network, and your insurance plan does not cover the full cost of the service. It often happens even if you thought you were covered.

Surprise billing is a type of balance billing that you did not expect. It usually means you could not choose the provider or know the provider’s network status when you received care. For example, you might go to an in-network facility for care, but a radiologist or laboratory service that treats you is out-of-network, and then you get a bill that you did not plan for.

In Texas, state law and the federal No Surprises Act (NSA) work to protect patients from unexpected bills. Texas law applies to state-regulated health plans if your insurance card shows “TDI” or “DOI.” The No Surprises Act is a federal law that also protects many people, especially those with group health insurance or self-funded plans.

Under these protections, you usually only pay your normal copayment, deductible, and coinsurance for emergency care or when you cannot choose your provider. Your insurer and the provider must settle the remaining balance without sending you a large bill. If they cannot agree, there may be a process, such as Independent Dispute Resolution (IDR), to help resolve the payment issue.

In simple terms:

- Balance billing is the practice of billing you the difference between what your plan pays and what the provider charges.

- Surprise billing is a balance bill you did not expect because you had no choice of provider or did not know about the network status.

These rules protect many Texans, especially when you go to an in-network place but see an out-of-network provider, or when you need emergency ambulatory care without a chance to check network status.

Overview of Texas Surprise Billing Laws

Texas has rules to protect you from surprise bills and balance billing when you get medical care. These rules come from Texas state law and work with federal laws, such as the No Surprises Act (NSA), to limit what you pay when you don’t have a real choice of providers.

What Texas Law Does

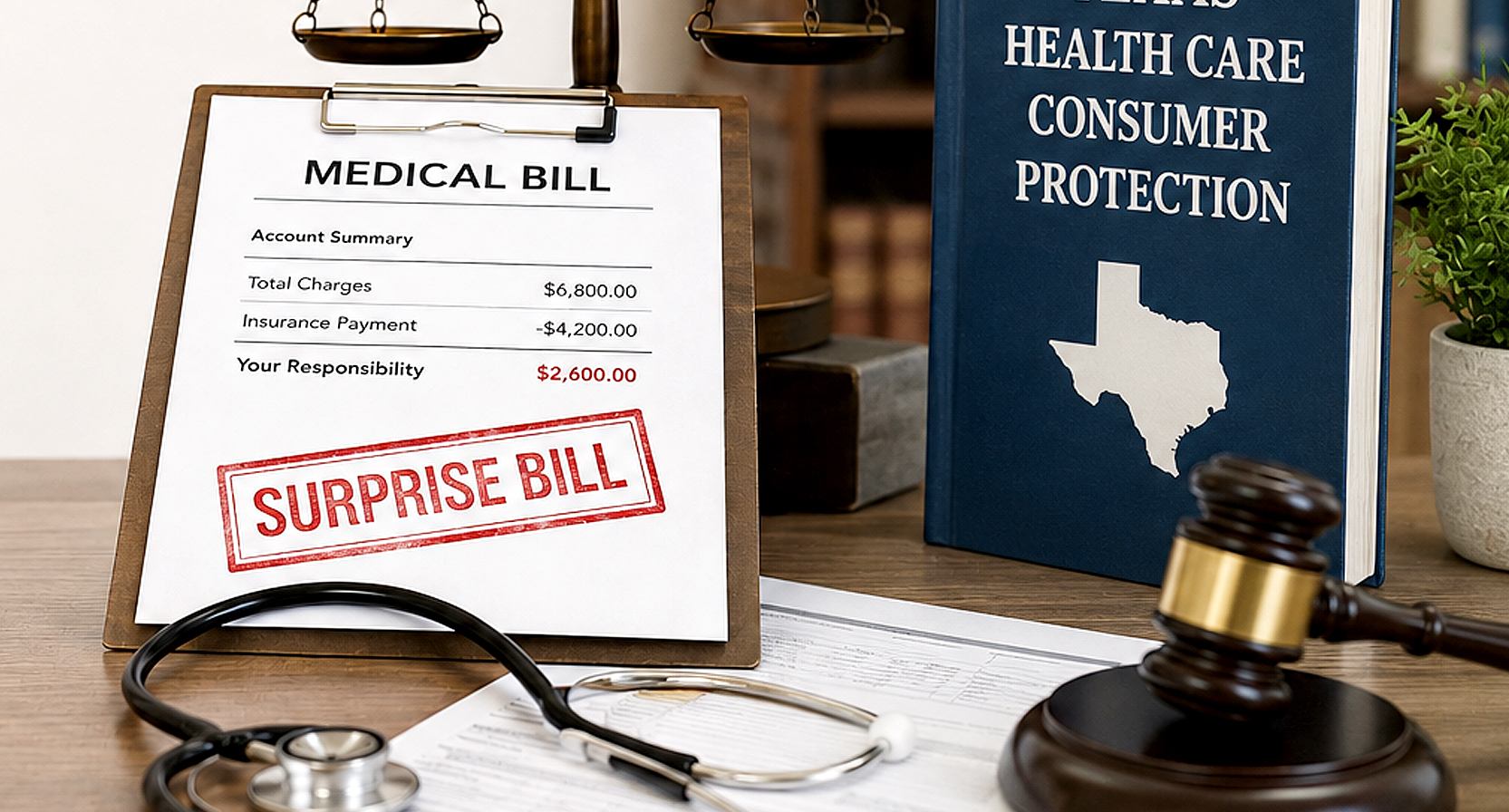

Texas law bans balance billing for people with state-regulated health plans in many situations. These protections started on January 1, 2020, with Senate Bill 1264, and they are part of the Texas Insurance Code that the Texas Department of Insurance (TDI) enforces.

Here’s how it works:

- If you have a state-regulated health plan (your insurance card shows TDI or DOI, or you are in an Employee Retirement System (ERS) or Teacher Retirement System (TRS) plan, Texas law limits balance billing for many services.

- You will generally pay only your copayment, deductible, and coinsurance – just like if you saw an in-network provider.

- Providers cannot send you a surprise medical bill if you did not choose them and you are under a protected plan.

Texas law also requires out-of-network doctors and facilities to use a mediation or arbitration process if they do not agree on payment with your insurer, instead of billing you directly.

Who Is Protected

You are covered by Texas surprise billing and balance billing protections if:

- Your health plan is state-regulated (look for TDI or DOI on your insurance card).

- You are covered under an ERS or TRS plan.

These protections may not apply if your employer’s plan is self-funded (ERISA), unless it has opted in to participate in Texas dispute resolution rules. In that case, federal protections still apply.

Services Covered by Texas Law

Texas surprise billing rules stop most balance billing when:

- You get emergency care, even if the emergency room or provider is out-of-network.

- You get services at an in-network facility, but a doctor, such as an anesthesiologist or radiologist, is out-of-network.

- You are transported by ground ambulance in emergencies (new protections effective in recent years).

For plans subject to federal law, the No Surprises Act also bans balance billing for air ambulances and similar services.

Exceptions & When Balance Billing Still Happens

Even though Texas’s surprise billing and balance billing rules protect many patients, balance billing can still happen in certain situations. Knowing when these exceptions apply can help you avoid surprise medical bills.

State vs. Federal Rules

Texas law, including Senate Bill 1264 and parts of the Texas Insurance Code, bans most surprise billing for people with state-regulated health plans. This includes plans with TDI or DOI on the card, such as the Employee Retirement System (ERS) and the Teacher Retirement System (TRS).

Federal rules under the No Surprises Act (NSA) also protect people with many private plans from balance billing after January 1, 2022. These federal protections generally cover group plans, individual plans, and certain emergency care.

When Balance Billing Can Still Happen

Here are the main exceptions where providers might bill you beyond your in-network cost share:

1. Self-Funded Employer Plans (ERISA)

If your health plan is self-funded and operates under federal rules (ERISA), Texas state protections may not apply unless the plan has opted in to the state’s dispute-resolution processes.

2. You Choose Out-of-Network Care

If you knowingly select an out-of-network provider in a non-emergency (for example, you pick an out-of-network doctor at an in-network hospital), protections may not block balance billing.

3. Written Consent or Waiver

In some non-emergency cases, a provider may ask you to sign a waiver or informed consent form that lets them bill you more than in-network costs. If you sign it, state protections may not apply to that service.

4. Non-Emergency Care at Out-of-Network Facilities

If you go to a facility that is fully out-of-network, and you agree to that choice, balance billing may be allowed.

Important Notes on Exceptions

- Emergency services are almost always protected, even with an out-of-network provider, unless you give up protections in writing after care.

- Texas protections often match or build on the No Surprises Act, so you are usually protected for key services like emergency care, and when you did not choose an out-of-network provider.

- If there is a dispute between a provider and your insurance plan about payment, they must use the Independent Dispute Resolution (IDR) process instead of billing you extra.

Understanding these exceptions helps you see when Texas law and federal law might not stop balance billing and what you can expect if you get care outside your insurance network. Let me know when you’re ready for the next section on “How Dispute Resolution Works.”

How Dispute Resolution Works

When a surprise medical bill or balance billing issue happens in Texas, you often do not pay the extra charges yourself. Instead, your health plan and the out-of-network provider work through a formal process to resolve payment disagreements. This process, called Independent Dispute Resolution (IDR), includes mediation and arbitration.

What Independent Dispute Resolution Means

IDR is a system where a neutral third party reviews the case when a health plan and an out-of-network provider cannot agree on how much the plan should pay for services. In Texas, state law requires this process instead of letting the provider send you a large balance bill.

Two Main Tracks: Mediation and Arbitration

Texas law uses two main types of dispute resolution, depending on the kind of provider involved:

- Mediation is used to resolve billing disputes between out-of-network facilities (such as hospitals) and health plans.

- Arbitration is used when disputes involve out-of-network health care providers (such as doctors, radiologists, or labs) and health plans.

How the Process Works

Here’s a simple view of how dispute resolution usually works:

- The health plan makes a first payment or explains why it paid a certain amount.

- If the provider disagrees with the amount paid, they may try to resolve the issue directly with the insurer.

- If they still do not agree, the provider (or facility) can request IDR through the Texas Department of Insurance (TDI) IDR portal.

- At first, there is an informal period where both sides can settle the case on their own.

- If they cannot settle, a mediator (for facilities) or an arbitrator (for providers) reviews the case and decides on payment.

- The decision helps determine how much the health plan pays and what the provider accepts, so you avoid a big surprise bill.

Deadlines and Rules

Under Texas law, if neither side agrees early, there are timelines they must follow:

- Mediation requests must be made within 180 days of the first claim payment or denial.

- Arbitration also has specific windows (e.g., 20-90 days after the first payment) for providers to initiate the process.

Why This Protects You

IDR puts you in the middle of a fight between your insurance plan and the out-of-network provider. Instead of you paying the billed charges beyond your deductible, copay, or coinsurance, the dispute resolution system decides a fair payment amount.

Where IDR Comes From

Texas laws, including Senate Bill 1264 and Texas Insurance Code Chapter 1275, include rules for balance billing prohibitions and out-of-network claim dispute resolution. These rules work with federal protections like the No Surprises Act to protect patients from surprise bills and give a formal way to resolve disputes without burdening you.

What To Do If You Receive a Surprise Bill

If you get a surprise medical bill or a balance bill in Texas, don’t panic. You have rights and ways to handle it. These steps show you what to do next so you don’t pay more than you should under Texas surprise billing and balance billing rules and the No Surprises Act (NSA).

1. Check Your Bill and Explanation of Benefits (EOB)

- Look at the bill carefully and compare it with your Explanation of Benefits (EOB) from your insurance.

- See if the charges are from an out-of-network provider or an in-network facility, and if the bill matches what your insurer paid.

- If the provider billed you more than your copayment, deductible, or coinsurance for a covered service, this may be balance billing that is not allowed under the law.

2. Contact Your Insurance Plan

- Call your health plan’s customer service.

- Ask why the service was billed that way and whether it should count as an in-network cost under Texas rules or the No Surprises Act.

- Sometimes claims are coded incorrectly, and a corrected claim can fix the mistake.

3. Contact the Provider Who Billed You

- Ask the health care provider or facility to explain the bill.

- Make sure they know your plan type and that the law may protect you from balance billing if you had no choice of provider.

- If it were truly a surprise billing situation, providers should work with your plan through Independent Dispute Resolution (IDR) or other processes instead of billing you directly.

4. File a Complaint or Appeal

- If your insurance plan denies your appeal or you think you were billed incorrectly, you can file a complaint:

- With the Texas Department of Insurance (TDI) at 800-252-3439 or online through the consumer protection page.

- With your health plan through its formal appeal process.

- Be sure to include copies of the bill, the EOB, and any letters you have from your insurer and provider.

5. Ask for Help if Needed

- If you find the process confusing, you can get help from:

- The TDI Consumer Protection Division for Texas addresses surprise billing issues.

- A medical billing advocate or lawyer who understands balance billing and surprise medical bills.

- They can help make sure your rights under Texas law and the No Surprises Act are respected.

Common Scenarios (Examples)

Here are some real-life examples of how Texas’s surprise billing and balance billing rules work in practice. These help show when you should be protected from a big bill and when a balance bill might still occur.

Scenario 1: Emergency Room Visit with an Out-of-Network Doctor

If you go to an in-network hospital for sudden chest pain and an out-of-network physician treats you, the provider cannot balance bill you for the difference between their charge and what your plan pays. You only owe your deductible, copay, and coinsurance.

This rule applies because emergency care is one of the clearest examples where you had no choice about which doctor you saw.

Scenario 2: Out-of-Network Specialist at an In-Network Facility

You schedule a gallbladder surgery at a hospital that is in your network. The surgeon is in network, but an assistant surgeon or anesthesiologist who participates in your care is out of network. In this case, you still pay only your normal in-network cost share for all services.

This type of surprise bill used to be common, but under Texas balance billing rules, your insurer treats the charges as in-network for your cost-sharing, and the provider must settle with the plan.

Scenario 3: Diagnostics or Lab Work You Didn’t Choose

At an “in-network” hospital, you might have your bloodwork, radiology, or imaging done by an out-of-network provider without realizing it. In Texas, this also falls under surprise billing protections, so you generally will not be billed beyond your in-network cost share.

Scenario 4: Ground Ambulance Ride After an Accident

For many years, ground ambulance services were not always protected under federal law. Texas extended its own protections so that if you are taken by a ground ambulance in an emergency, your plan must cover it like an in-network service, and you don’t owe a big additional bill beyond your plan share.

This matters because ambulance bills can be very large and happen without any choice.

Scenario 5: Air Ambulance Transport

If you are air-lifted by an emergency air ambulance, federal law now protects most patients from being balance billed for air ambulance services. You pay only your in-network cost share, and the insurer and provider resolve payment behind the scenes if needed.

Scenario 6: You Choose an Out-of-Network Provider

If you knowingly choose to see an out-of-network specialist for a non-emergency procedure, and you sign a Balance Billing Waiver, you may be responsible for charges beyond what your plan would normally pay. This is an example of a situation where protections do not apply if you agreed to them.

Scenario 7: Self-Funded Employer Plan Without Opt-In

Some large employer plans are self-funded under ERISA and are not fully covered by Texas state rules unless the employer has opted into Texas’s dispute resolution system. In this case, the federal No Surprises Act still offers baseline protections, but the specific Texas dispute-resolution rules (such as certain mediation and arbitration rules) may not apply.

These scenarios show common ways Texans can end up with surprise bills, and when the Texas surprise billing law, No Surprises Act, and Texas balance billing rules protect patients from large unexpected charges.

Frequently Asked Questions (FAQs)

Q: What is balance billing?

Balance billing is when a health care provider bills you the difference between what your insurance pays and the total charge for a medical service. This often happens when the provider is out-of-network.

Q: What is surprise billing?

Surprise billing is a balance bill you did not expect, usually because you could not control which out-of-network provider treated you at an in-network facility or in an emergency.

Q: Does Texas law protect me from surprise medical bills?

Yes. Texas bans balance billing for many emergency services and for out-of-network providers at in-network facilities if you have a state-regulated health plan.

Q: What does the federal No Surprises Act do?

The No Surprises Act protects patients in many plans from balance billing for emergency services and certain non-emergency services from out-of-network providers, including air ambulance services, starting January 1, 2022.

Q: What if my plan is self-funded under ERISA?

If your plan is ERISA and doesn’t opt into Texas IDR rules, you are still protected under the federal No Surprises Act for many surprise billing situations.

Q: What should I do if I get a surprise bill?

Check your bill and the insurer’s Explanation of Benefits, contact your insurer and provider, and if needed, file a complaint with the Texas Department of Insurance or use the dispute processes available.

Q: Are ambulance services covered?

Texas law now protects ground ambulance services from balance billing in many cases, and the No Surprises Act covers air ambulance services against balance billing.